All Categories

Featured

Table of Contents

[/video]

When the main annuity holder dies, a picked beneficiary remains to get either 50% or 100% of the revenue permanently. 60 years 6,291.96 6.29% Criterion Life 65 years 6,960.24 6.96% Canada Life 70 years 7,776.60 7.78% Canada Life 75 years 8,941.56 8.94% Canada Life The existing ideal 50% joint life annuity rate for a 65-year-old man is 6.96% from Canada Life, which is 0.24% less than the very best price in February.

describes the individual's age when the annuity is established. These tables reveal annuities where earnings payments continue to be degree throughout of the annuity. Rising strategies are likewise readily available, where repayments begin at a lower degree yet enhance yearly according to the Retail Costs Index or at a fixed rate.

For both joint life instances, numbers shown are based on the first life being male, and the beneficiary being a woman of the very same age. Single life, degree 7,545.60 7,554.12 7,458.72 7,496.40 7,435.08 7,444.92 Single life, rising at 3% 5,390.40 5,399.16 5,341.80 5,425.80 5,673.36 5,535.84 Single life, intensifying at RPI 4,795.92 4,804.80 4,722.96 4,778.28 5,067.96 4,946.16 Joint life 50% 6,952.92 6,960.96 6,834.12 6,896.76 7,143.84 7,064.64 Joint life 100% 6,385.68 6,392.64 6,262.92 6,318.60 6,683.76 6,691.80 Information on historic annuity prices from UK companies, generated by Retirement Line's in-house annuity quote system (typically at or near the very first day of each month).

On top of that: is where payments begin at a lower degree than a degree plan, but rise at 3% yearly. is where repayments begin at a reduced level than a level plan, but enhance every year in line with the Retail Rate Index. Utilize our interactive slider to demonstrate how annuity prices and pension plan pot dimension affect the revenue you can receive: Annuity rates are a crucial element in identifying the level of revenue you will certainly get when purchasing an annuity with your pension plan cost savings.

The greater annuity rate you safeguard, the more income you will certainly get. For instance, if you were purchasing a life time annuity with a pension fund of 100,000 and were offered an annuity rate of 5%, the yearly income you receive would be 5,000. Annuity prices vary from service provider to carrier, and companies will certainly provide you a personal rate based upon a variety of elements consisting of underlying economic aspects, your age, and your wellness and way of living for lifetime annuities.

This provides you certainty and reassurance concerning your long-lasting retired life revenue. Nevertheless, you could have an intensifying life time annuity. This is where you can select to begin your payments at a lower level, and they will after that enhance at a fixed portion or according to the Retail Cost Index.

Jackson Annuity Rates

With both of these choices, once your annuity is set up, it can not usually be transformed., the price stays the same until the end of the selected term.

It may amaze you to discover that annuity prices can vary dramatically from provider-to-provider. At Retirement Line we have actually found a difference of as much as 15% in between the least expensive and highest prices readily available on the annuity market. Retirement Line specialises in providing you a comparison of the most effective annuity prices from leading carriers.

(also recognized as gilts) to fund their clients' annuities. This in turn funds the normal income payments they make to their annuity clients. Suppliers money their annuities with these bonds/gilts because they are among the safest types of investment.

The gilt return is connected to the Financial institution of England's Financial institution Price, additionally called the 'base price' or 'rate of interest price'. When the Bank Rate is reduced, gilt yields are additionally low, and this is shown in the pension plan annuity rate. On the various other hand, when the Financial institution Rate is high, gilt yields and common annuity rates likewise tend to increase.

Also, annuity companies utilize added economic and commercial factors to identify their annuity prices. This is why annuity prices can increase or drop despite what occurs to the Bank Price or gilt returns. The vital thing to bear in mind is that annuity rates can alter frequently. They additionally normally differ from provider-to-provider.

Annuity Taxes After Death

This was of course great information to individuals who were prepared to transform their pension plan pot right into a surefire income. Canada Life's record at that time pointed out a benchmark annuity for a 65-year-old utilizing 100,000 to acquire an annuity paying an annual life time income of 6,873 per year.

This is since providers will not just base your rate on your age and pension plan fund dimension. They will rather base it on your individual personal circumstances and the sort of annuity you desire to take. This information is for illustratory functions only. As we have described above, your annuity service provider will base their annuity rate on financial and commercial variables, consisting of existing UK gilt yields.

American General Fixed Annuity

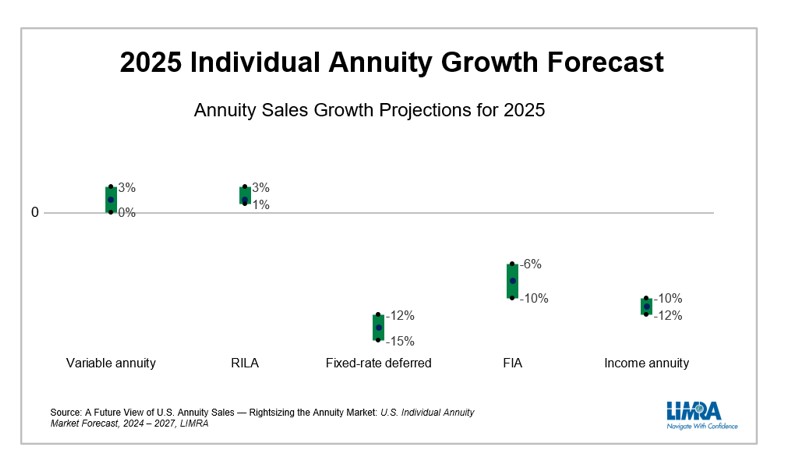

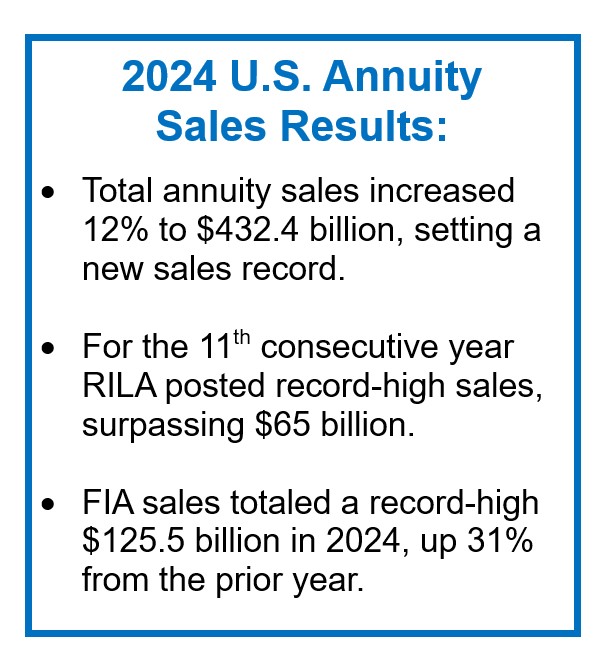

To place this right into viewpoint, that's almost double the sales in 2021. In 2025, LIMRA is predicting FIA sales to drop 5%-10% from the document embeded in 2024 yet continue to be above $100 billion. RILA sales will certainly note its 11th successive year of record-high sales in 2024. Capitalists thinking about protected development paired with proceeded strong equity markets has actually made this item popular.

LIMRA is predicting 2025 VA sales to be level with 2024 outcomes. After record-high sales in 2023, income annuities thrust by compelling demographics trends and appealing payout prices should exceed $18 billion in 2024, setting another record. In 2025, reduced rates of interest will certainly force carriers to drop their payout rates, causing a 10% cut for earnings annuity sales.

Annuity Transfer On Death

It will be a combined expectation in 2025 for the general annuity market. While market conditions and demographics are really favorable for the annuity market, a decrease in rate of interest (which drove the impressive growth in 2023 and 2024) will certainly undercut fixed annuity items continued growth. For 2024, we expect sales to be greater than $430 billion, up between 10% to 15% over 2023.

The company is additionally a struck with representatives and clients alike. "Allianz is remarkable," John Stevenson, owner and expert at Stevenson Retirement Solutions, told Annuity.org. "They're A+ rated. A great deal of my clients like that and they're eager to accept a bit reduced of an earnings due to the fact that of that.

The business rests atop the most current edition of the J.D. Power Overall Client Contentment Index and flaunts a strong NAIC Grievance Index Score, too. Pros Market leader in client complete satisfaction More powerful MYGA rates than a few other very ranked business Cons Online product info might be more powerful A lot more Insights and Specialists' Takes: "I have actually never had a disappointment with them, and I do have a couple of delighted clients with them," Pangakis said of F&G.

The firm's Secure MYGA includes advantages such as bikers for incurable ailment and assisted living home arrest, the capability to pay out the account worth as a survivor benefit and rates that surpass 5%. Few annuity business succeed greater than MassMutual for consumers that value monetary toughness. The company, established in 1851, holds a distinguished A++ ranking from AM Best, making it one of the best and best firms readily available.

Its Steady Trip annuity, for example, gives a traditional way to generate revenue in retired life matched with manageable abandonment costs and different payment choices. The business also promotes registered index-linked annuities through its MassMutual Ascend subsidiary.

Computer Patent Annuities

"Nationwide attracts attention," Aamir Chalisa, basic manager at Futurity First Insurance Group, informed Annuity.org. "They've obtained amazing customer care, a very high ranking and have been around for a variety of years. We see a great deal of customers asking for that." Annuities can supply considerable worth to prospective customers. Whether you intend to produce earnings in retirement, grow your money without a great deal of danger or benefit from high prices, an annuity can efficiently achieve your objectives.

Annuity.org laid out to recognize the leading annuity firms in the sector. To accomplish this, we developed, checked and executed a fact-based approach based upon vital sector aspects. These include a firm's monetary stamina, schedule and standing with customers. We likewise got in touch with multiple market professionals to get their handles various firms.

{kind=link}

Latest Posts

Annuity Leads For Sale

Variable Annuity With Income Rider

Creditor Protection Annuities By State